Millions struggle with high-interest debt while juggling multiple payments. A credit union consolidation loan offers a potential solution by combining these debts into a single, lower-interest payment. However, eligibility requirements and associated fees vary widely. Careful consideration is crucial before pursuing this option.

Toc

- 1. Understanding Credit Union Consolidation Loans: A Comprehensive Guide

- 2. Related articles 01:

- 3. Comparing Debt Consolidation Strategies

- 4. Current Trends in Debt Consolidation

- 5. Maximizing Your Credit Union Consolidation Loan Benefits

- 6. Finding the Best Credit Union for Debt Consolidation

- 7. Credit Union Consolidation Loan for Bad Credit

- 8. Advanced Considerations for Debt Consolidation

- 9. Conclusion: Your Path to Financial Simplification

- 10. Related articles 02:

Understanding Credit Union Consolidation Loans: A Comprehensive Guide

Credit union consolidation loans represent a powerful financial strategy for individuals overwhelmed by multiple high-interest debts. Unlike traditional bank loans, these specialized financial products offer a unique approach to debt management that can potentially save borrowers significant money over time.

What Makes Credit Union Consolidation Loans Unique?

A credit union consolidation loan allows borrowers to:

- Combine multiple existing debts into a single payment

- Potentially lower overall interest rates

- Simplify monthly financial tracking

- Benefit from member-focused, non-profit organizational structures

Credit unions distinguish themselves from traditional banks by providing more personalized services and often more competitive rates. Their non-profit status enables them to offer more flexible terms that prioritize member financial well-being.

In addition to these advantages, it’s essential to consider the potential tax implications of debt consolidation loans. While interest paid on personal loans is generally not tax-deductible, certain situations—such as home equity loans used specifically for home improvements—might offer exceptions. Understanding these nuances can aid in making informed financial decisions.

The Mechanics of a Credit Union Consolidation Loan

Credit unions simplify debt by providing a new loan to pay off existing balances. This process transforms multiple payments into a single monthly obligation, making financial management more straightforward. Here’s how it typically works:

- Loan Application: You apply for a loan from a credit union, which often involves submitting personal and financial information.

- Approval and Funding: Once approved, the credit union disburses the loan amount directly to your creditors, effectively paying off your existing debts.

- Single Monthly Payment: You will then make one monthly payment to the credit union at a potentially lower interest rate than what you were previously paying.

- Improved Financial Management: This method not only simplifies your financial obligations but can also provide an opportunity to improve your credit score over time, provided you make timely payments.

When considering a credit union consolidation loan, understanding the eligibility requirements is vital. This section is broken down into key categories:

1. https://khositrangsuc.com/mmoga-sofi-loan-consolidation-your-guide-to-simplifying-debt/

3. https://khositrangsuc.com/mmoga-va-loan-pre-approval-your-step-by-step-guide/

4. https://khositrangsuc.com/mmoga-find-the-best-small-business-line-of-credit-loan/

5. https://khositrangsuc.com/mmoga-parent-plus-loan-consolidation-your-complete-guide/

Credit Score Considerations

Most credit unions require a minimum credit score, which can vary depending on the lender and the loan amount. If your credit score is on the lower end, it’s essential to explore options tailored for bad credit. Many credit unions have specialized programs to assist borrowers with less-than-perfect credit histories.

Income and Debt-to-Income Ratio

You will need to provide proof of stable income, which can include pay stubs, tax returns, or bank statements. A debt-to-income ratio (DTI) below a certain percentage is often required, typically around 40% to 50%. This ratio helps lenders assess your ability to repay the loan effectively.

Other Eligibility Factors

Credit unions may also consider other factors such as residency requirements, employment history, and membership criteria. Being a member of a credit union can often lead to more favorable terms, so it’s worth exploring membership options if you haven’t already.

Credit Union Consolidation Loan Application Process

Successfully applying for a credit union consolidation loan involves several important steps:

- Gathering Documentation: Collect all necessary financial documents, including income verification, details of your existing debts, and identification.

- Completing the Application: Fill out the application either online or in person. It’s crucial to provide complete and accurate information to avoid delays in approval.

- Using a Credit Union Consolidation Loan Calculator: Many credit unions provide online calculators to help you estimate potential monthly payments and overall savings based on different loan amounts and terms.

- Understanding Credit Impacts: Be aware that applying for a loan may result in a hard inquiry on your credit report, which can temporarily lower your credit score. However, making consistent, on-time payments can lead to an improvement in your score over time.

- Monitoring Your Credit Score: After applying, it’s important to monitor your credit score regularly. Even with approval, the hard inquiry can impact your score. Utilizing resources like annualcreditreport.com allows you to check your credit report for free and stay informed about any changes.

Comparing Debt Consolidation Strategies

When exploring debt consolidation, it’s essential to compare various debt relief strategies to determine the best fit for your financial situation.

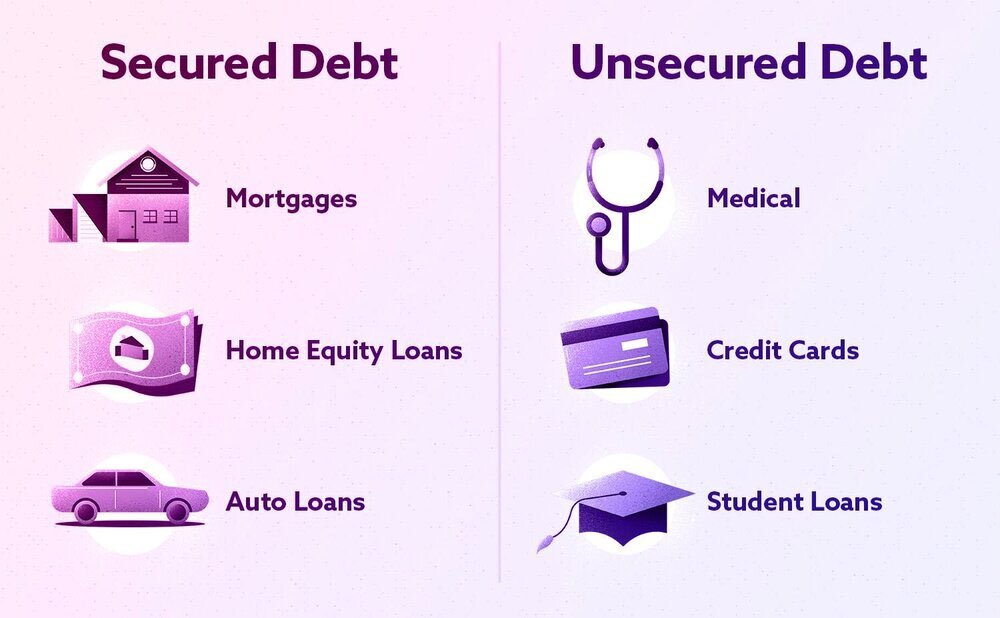

Alternative Debt Relief Options

- Balance Transfers:

- Pros: Balance transfers allow you to move high-interest credit card debt to a new card with a lower interest rate, potentially saving you money on interest.

- Cons: These often come with fees and may require excellent credit to qualify for the best offers. Additionally, the introductory rates may expire, leading to higher rates if balances are not paid off in time.

- Debt Management Programs:

- These programs involve working with a credit counseling agency to negotiate lower interest rates with your creditors. While this can provide relief, it typically requires a commitment to a structured repayment plan, which may impact your credit score.

- Bankruptcy:

- While bankruptcy can offer a fresh start, it has long-term consequences on your credit and financial future. It should only be considered as a last resort after evaluating other options.

- Credit Union Consolidation Loans:

- These loans often provide lower interest rates than credit cards and allow for flexible repayment terms. They can improve your credit profile if managed responsibly, making them a viable option for many budget-conscious individuals.

Comparing to Personal Loans

In addition to credit union consolidation loans, personal loans from banks or online lenders can also be considered. Credit unions often have more lenient requirements and may offer better rates for members with established relationships. However, bank loans might provide higher loan amounts or more specialized terms, making it essential to weigh the pros and cons of each option based on your individual circumstances.

Current Trends in Debt Consolidation

With the rise of online credit unions and fintech platforms, consumers now have more options than ever for debt consolidation loans. These digital lenders offer convenience and the potential for competitive rates. However, caution is warranted, as less-established lenders may pose risks that consumers should carefully evaluate before proceeding.

Maximizing Your Credit Union Consolidation Loan Benefits

Strategic Financial Management Techniques

Once you have secured a credit union consolidation loan, effective management of your monthly payments is crucial. Here are some strategies to help you stay on track:

- Creating a Comprehensive Budget:

- Establish a budget that accommodates your new payment plan. This involves tracking your spending to identify areas where you can cut back and allocate more towards your loan payments.

- Making Consistent, Timely Payments:

- Ensure that you make your loan payments on time each month. This not only helps you avoid late fees but also builds your credit history positively. However, it’s crucial to remember that inconsistent payments can negatively impact your credit score, highlighting the importance of financial discipline.

- Avoiding Additional Debt Accumulation:

- While repaying your consolidation loan, avoid taking on new debt. This can lead to a cycle of debt that is hard to escape. Instead, focus on living within your means and using the consolidation loan as a stepping stone towards financial stability.

Understanding Potential Risks

When considering a credit union consolidation loan, it’s important to be aware of potential risks:

- Initial Credit Score Fluctuations:

- Applying for a credit union consolidation loan may initially impact your credit score due to the hard inquiry performed by the lender. However, if you make consistent, on-time payments, you can improve your credit score over time.

- Prepayment Penalties:

- Some credit unions may charge prepayment penalties, which could affect your ability to pay off the loan early. Always read the loan agreement carefully to understand any fees associated with early repayment.

- Long-Term Financial Commitment:

- A consolidation loan can help you manage your debts, but it’s essential to consider the long-term implications of taking on new debt. Ensure that you’re not simply shifting your debt around without addressing the underlying financial habits that led to the debt accumulation in the first place.

Finding the Best Credit Union for Debt Consolidation

Research and Comparison Strategies

Finding the right credit union for your consolidation loan is critical to securing favorable terms. Here are key evaluation factors to consider:

- Interest Rates (APR):

- Compare the annual percentage rates offered by different credit unions. Look for the lowest rates to maximize your savings.

- Loan Terms:

- Review the loan terms, including repayment periods and any associated fees. Some credit unions may offer flexible repayment options that can cater to your financial situation.

- Customer Service Quality:

- Evaluate the customer service reputation of potential credit unions. Look for institutions known for their responsive and helpful service, as this can make a significant difference during the loan process.

Leveraging Online Resources

In today’s digital age, there are numerous resources available to help you find the best credit union for debt consolidation:

- Reddit Discussions:

- Online platforms like Reddit provide valuable insights into real-world experiences with credit union consolidation loans. Search for threads discussing “credit union consolidation loan reddit” to learn from others’ experiences and recommendations.

- Financial Review Websites:

- Websites dedicated to financial reviews often feature comprehensive comparisons of various credit unions. Look for sites that provide detailed ratings and customer feedback.

- Credit Union Comparison Tools:

- Use online comparison tools to evaluate multiple credit unions side by side. These tools can help you assess interest rates, fees, and loan terms quickly.

Credit Union Consolidation Loan for Bad Credit

Specialized Lending Options

If you have a less-than-ideal credit score, securing a credit union consolidation loan may still be possible. Many credit unions offer specialized programs designed for individuals with bad credit. Here are some options to consider:

- Specialized Loan Programs:

- Some credit unions have specific loan products tailored for borrowers with poor credit. These loans may come with higher interest rates, but they provide a pathway to consolidate debts and improve credit over time.

- Co-Signer Opportunities:

- If you have a trusted friend or family member with good credit, consider asking them to co-sign your loan. This can improve your chances of approval and may help you secure better loan terms.

- Gradual Credit Rebuilding Strategies:

- Once you secure a loan, make timely payments to gradually rebuild your credit score. Over time, this can open up opportunities for better financial products and lower interest rates.

Advanced Considerations for Debt Consolidation

Utilizing Consolidation Loan Calculators

One of the most valuable tools at your disposal when considering a credit union consolidation loan is the loan calculator. Here’s how to use it effectively:

- Projected Monthly Payment Estimates:

- Enter your desired loan amount, interest rate, and loan term to see what your monthly payments will look like. This can help you budget effectively and determine what you can afford.

- Total Interest Savings Calculations:

- Many calculators will show you the total interest you’ll pay over the life of the loan. This information can help you compare loans and choose the most cost-effective option.

- Loan Term Comparison Tools:

- Use the calculator to experiment with different loan terms. Shorter terms may come with higher monthly payments but lower overall interest costs.

Community Insights and Experiences

Engaging with online communities can provide valuable insights into the credit union consolidation loan process. Here are some ways to leverage community knowledge:

- Real-World Loan Experiences:

- Join forums or discussion groups where individuals share their experiences with credit union loans. This can provide you with practical tips and warnings based on real-life situations.

- Insider Tips from Past Borrowers:

- Learn from the mistakes and successes of others. Many individuals are willing to share what worked for them and what pitfalls to avoid.

- Unfiltered Credit Union Reviews:

- Use platforms like Reddit to find unfiltered reviews of credit unions. This can help you identify which institutions have a solid reputation and which may not meet your needs.

Conclusion: Your Path to Financial Simplification

A credit union consolidation loan can significantly simplify debt management and potentially save you money on interest. By carefully selecting a credit union, understanding the requirements, and employing responsible borrowing practices, you can take control of your finances and work towards a debt-free future.

Key takeaways include:

- Research multiple credit unions to find the best fit for your needs.

- Understand your financial situation and eligibility requirements.

- Use online resources and community insights to guide your decision-making process.

- Maintain disciplined repayment strategies to maximize your savings and improve your credit score.

Take the first steps towards financial freedom today by exploring credit union consolidation loan options tailored to your unique circumstances. By making informed choices and leveraging available resources, you can pave the way for a more secure financial future.

2. https://khositrangsuc.com/mmoga-sofi-loan-consolidation-your-guide-to-simplifying-debt/

3. https://khositrangsuc.com/mmoga-parent-plus-loan-consolidation-your-complete-guide/

4. https://khositrangsuc.com/mmoga-va-loan-pre-approval-your-step-by-step-guide/

5. https://khositrangsuc.com/mmoga-find-the-best-small-business-line-of-credit-loan/