Recent changes in income-driven repayment plans, including the SAVE plan, offer new possibilities for Parent PLUS loan borrowers. Consolidation can unlock access to these plans, potentially leading to lower monthly payments and loan forgiveness. However, the process is complex, and the July 1, 2025 deadline adds urgency.

Toc

- 1. Understanding Parent PLUS Loans and Their Challenges

- 2. The Benefits of Parent PLUS Loan Consolidation

- 3. Direct Consolidation Loan Process: A Step-by-Step Guide

- 4. Income-Driven Repayment Plans After Consolidation

- 5. Related articles 01:

- 6. The Parent PLUS Loan Consolidation Loophole: Accessing SAVE and Other IDR Plans

- 7. Risks and Challenges of Double Consolidation and Alternatives

- 8. Current Trends Impacting Parent PLUS Borrowers

- 9. Tips, Best Practices, and Actionable Steps for Parent PLUS Loan Consolidation

- 10. Conclusion: Take Control of Your Parent PLUS Loan Debt Today

- 11. FAQ Section

- 12. Related articles 02:

- 13. Additional Information and Resources

- 14. Final Thoughts

Understanding Parent PLUS Loans and Their Challenges

Parent PLUS loans are federal loans designed for parents who wish to assist their dependent undergraduate children with college expenses. These loans are available to biological, adoptive, and stepparents, providing a vital funding option for education. However, they come with notable challenges that many parents struggle to navigate.

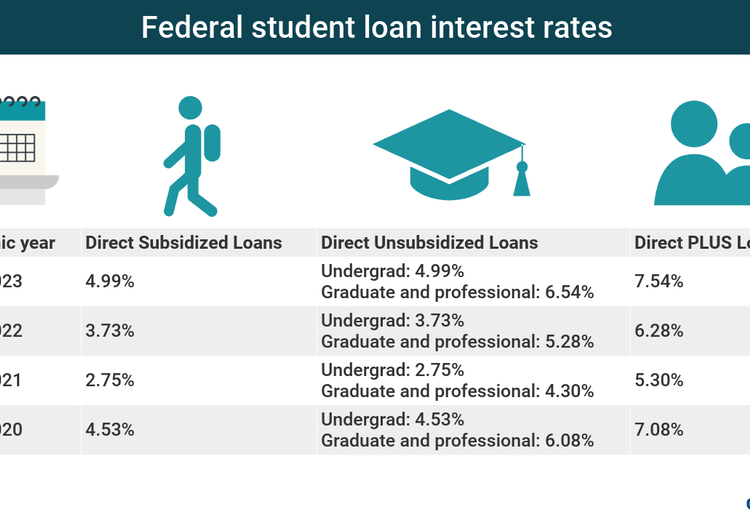

One significant hurdle is the interest rate, which currently stands at 7.54% as of 2024. This rate is notably higher than that of other federal student loans, creating a considerable financial burden for parents. Repayment can be particularly daunting, especially for those nearing retirement age, as they may face the dual challenge of managing debt while preparing for their future.

Another challenge lies in the repayment options available. Unlike other federal loans, Parent PLUS loans do not qualify for income-driven repayment plans unless they are consolidated into a Direct Consolidation loan. This limitation can leave parents feeling trapped under the weight of their financial obligations.

The emotional weight of this debt can be crushing, causing anxiety and stress that impacts a parent’s overall well-being. Moreover, late or missed payments can negatively affect credit scores, potentially hindering future financial opportunities such as obtaining mortgages or auto loans. Given these challenges, it becomes essential for borrowers to understand their options, including the potential for Parent PLUS loan consolidation.

The Benefits of Parent PLUS Loan Consolidation

Parent PLUS loan consolidation can provide a pathway to manage repayment more effectively. By consolidating these loans, parents can create a new Direct Consolidation loan, allowing access to a variety of repayment plans, including income-driven options that may significantly reduce monthly payments.

Streamlined Payments

Consolidation simplifies the repayment process by combining multiple Parent PLUS loans into one single loan. This can streamline monthly payments and make budgeting easier for families. Additionally, with a Direct Consolidation loan, borrowers gain access to several repayment plans tailored to their financial circumstances.

Access to Income-Driven Repayment Plans

One of the primary advantages of consolidation is the opportunity to enroll in income-driven repayment plans. These plans base monthly payments on a percentage of the borrower’s discretionary income, making them more manageable for those facing financial difficulties. This can lead to lower monthly payments, providing much-needed relief for struggling families.

However, it’s important to clarify that while consolidation simplifies repayment, it does not reduce the total interest paid over the life of the loan. For instance, consolidating two loans with $10,000 balances at 7% and 8% interest into one $20,000 loan might result in a weighted average interest rate of approximately 7.5%. While monthly payments may be easier to manage, the total interest paid will likely remain similar to the combined interest of the original loans.

Moreover, the consolidation process introduces the Parent PLUS loan consolidation loophole, which can be an essential strategy for accessing even more favorable repayment options.

Direct Consolidation Loan Process: A Step-by-Step Guide

If you’re considering Parent PLUS loan consolidation, understanding the application process is crucial. Here’s a detailed guide to help you navigate this journey.

Step 1: Gather Required Information

Before you begin the application process, ensure you have all necessary documents ready. This includes information about your existing Parent PLUS loans, such as loan balances, interest rates, and loan servicer details.

Step 2: Complete the Application

To initiate consolidation, you must fill out the Parent PLUS Loan Consolidation paper application. This application can be completed online through the Federal Student Aid website or via a paper form. It is crucial to ensure all information is accurate to avoid delays in processing.

Step 3: Understand the Interest Rate Calculation

Once your application is submitted, the interest rate for the new Direct Consolidation loan will be calculated. This rate is the weighted average of the loans being consolidated, rounded up to the nearest one-eighth percent. While this means that monthly payments may be lower, it’s important to note that the overall interest rate on the loan will not decrease.

Step 4: Choose a Repayment Plan

After consolidation, borrowers have the option to select from various repayment plans. Here are some of the available choices:

- Standard Repayment Plan: Fixed monthly payments over a 10-year term, which typically results in higher total interest paid over the life of the loan.

- Graduated Repayment Plan: Payments start low and increase every two years, suitable for those expecting their income to rise.

- Extended Repayment Plan: Allows for either fixed or graduated payments over 25 years, ideal for parents with larger loan balances.

- Income-Contingent Repayment (ICR) Plan: Payments are based on a percentage of discretionary income, offering a potential solution for those experiencing financial hardship.

Each of these options has its benefits and drawbacks, so it’s essential to consider your financial situation carefully before making a decision.

Income-Driven Repayment Plans After Consolidation

Once you have consolidated your Parent PLUS loans, you can explore income-driven repayment plans that can help ease your financial burden.

Income-Contingent Repayment (ICR) Plan

The ICR plan bases payments on a percentage of your discretionary income, which can provide immediate relief for those facing financial difficulties. However, it’s important to note that while this plan can lower your monthly payments, it is often the most expensive option in terms of total interest paid over the life of the loan.

1. https://khositrangsuc.com/mmoga-find-the-best-small-business-line-of-credit-loan/

3. https://khositrangsuc.com/mmoga-sofi-loan-consolidation-your-guide-to-simplifying-debt/

4. https://khositrangsuc.com/mmoga-va-loan-pre-approval-your-step-by-step-guide/

The SAVE Plan

The recently introduced Saving on a Valuable Education (SAVE) plan offers even more advantages. Under this plan, monthly payments can be as low as 10% of discretionary income, compared to the 20% required under the ICR plan. Additionally, the SAVE plan has provisions for loan forgiveness after 20 or 25 years of qualifying payments, depending on when the loans were taken out. However, it’s important to note that forgiveness under the SAVE plan is contingent upon continued qualifying payments, which may not result in complete loan forgiveness for all borrowers.

This potential for forgiveness can be a game-changer for borrowers who are struggling to keep up with high monthly payments.

The Parent PLUS Loan Consolidation Loophole: Accessing SAVE and Other IDR Plans

A critical strategy for those holding Parent PLUS loans is understanding the consolidation loophole that allows access to more favorable income-driven repayment plans, particularly the SAVE plan. This loophole can dramatically reduce monthly payment obligations and increase the potential for loan forgiveness.

The Double Consolidation Process

To take advantage of this loophole, borrowers must engage in a two-step consolidation process:

- First Consolidation: Begin by consolidating each Parent PLUS loan into separate Direct Consolidation loans. It’s advisable to use different loan servicers for each consolidation to meet eligibility requirements for the SAVE plan.

- Second Consolidation: Once you have two Direct Consolidation loans, the next step is to consolidate them into one final Direct Consolidation loan.

Completing this process before the July 1, 2025 deadline is crucial, as changes in legislation may restrict access to income-driven repayment plans for loans consolidated after this date.

Benefits of the SAVE Plan

The SAVE plan provides several benefits, including significantly lower payments based on a percentage of discretionary income. This can lead to substantial savings for many borrowers, making it an attractive option. Additionally, the SAVE plan offers loan forgiveness after 20 or 25 years of qualifying payments, depending on the borrower’s circumstances.

Risks and Challenges of Double Consolidation and Alternatives

While the double consolidation process can be advantageous, it is not without its challenges. The complexity of the process can lead to mistakes that may disqualify borrowers from accessing more favorable repayment plans.

Common Pitfalls to Avoid

Common pitfalls include submitting incorrect information or failing to meet deadlines. To mitigate these risks, it’s essential to stay organized and maintain a detailed record of all applications submitted.

Counterarguments to Double Consolidation

However, some financial advisors caution against the double consolidation strategy, citing the increased complexity and potential for errors. A single consolidation may be sufficient for many borrowers, especially those with simpler loan situations.

Alternatives to Consolidation: Refinancing

For some borrowers, refinancing may be a more suitable option than consolidation. Refinancing involves taking out a private loan to pay off Parent PLUS loans, potentially at a lower interest rate. However, it’s important to weigh the pros and cons carefully.

Pros and Cons of Refinancing

- Pros:

- Lower Interest Rates: Private lenders may offer lower rates than the fixed rates associated with Parent PLUS loans.

- Flexible Terms: Borrowers may have more flexibility in choosing loan terms that fit their financial situation.

- Cons:

- Loss of Federal Protections: Refinancing with a private lender means losing access to federal protections, including deferment, forbearance, and income-driven repayment plans.

- Eligibility Requirements: Many private lenders require good credit scores and stable incomes, which can be a barrier for some borrowers.

Additionally, some financial experts suggest considering the potential long-term implications of losing federal protections when deciding to refinance.

In addition to refinancing, borrowers can explore other strategies for managing Parent PLUS loan debt. This includes budgeting for extra payments, seeking financial counseling, or utilizing repayment assistance programs.

Current Trends Impacting Parent PLUS Borrowers

As of late 2023, there has been a pause on federal student loan repayments, a significant development that affects all federal student loan borrowers, including those with Parent PLUS loans. This extension of the payment pause has allowed borrowers additional time to prepare for the resumption of payments, but it also adds uncertainty regarding future repayment plans and interest rates.

Borrowers should regularly check official resources such as the Federal Student Aid website for updates on the status of loan repayments and any changes in legislation that could impact their financial responsibilities.

Tips, Best Practices, and Actionable Steps for Parent PLUS Loan Consolidation

If you’re considering Parent PLUS loan consolidation, here are some actionable steps to guide you through the process:

- Create a Checklist: Outline all required documents and forms needed for the consolidation application to ensure nothing is overlooked.

- Establish a Timeline: Aim to complete the double consolidation process well before the July 2025 deadline, allowing extra time for potential delays.

- Consult a Financial Advisor: Seek professional advice to help navigate the complexities of the consolidation process and select the right repayment plan.

- Utilize Online Resources : Explore forums and websites dedicated to student loan discussions, such as the Parent PLUS loan consolidation Reddit community, for additional support and insights from others in similar situations.

- Stay Informed: Keep abreast of any changes to federal student loan policies, as these can affect your repayment options and eligibility for forgiveness programs.

- Document Everything: Maintain a detailed record of all communications and applications related to your loans. This can be invaluable in resolving any issues that may arise during the consolidation process.

- Consider Group Support: Joining a support group or community can provide emotional support and practical advice from those who are also navigating Parent PLUS loan debt.

Resources for Financial Advisors and Support

Finding reputable financial advisors who specialize in student loan debt can be invaluable. Many organizations offer consultations to help borrowers understand their options and create tailored repayment plans.

Additionally, borrowers can access federal resources, such as the Federal Student Aid website, for information on the consolidation process, repayment options, and contact information for loan servicers.

Conclusion: Take Control of Your Parent PLUS Loan Debt Today

In conclusion, understanding the challenges of Parent PLUS loans and the options available for consolidation is essential for financial well-being. By leveraging strategies like double consolidation and exploring alternatives like refinancing, borrowers can work towards reducing their debt burden and achieving long-term financial stability.

Taking action now will empower parents to regain control over their finances and pave the way for a brighter future. If you are considering how to consolidate Parent PLUS loans to student , remember to explore all options, including the Parent PLUS loan consolidation loophole, and seek professional advice when needed. Don’t wait—act now to secure your financial well-being.

FAQ Section

Q: Are Direct Consolidation loans eligible for forgiveness?

A: Yes, Direct Consolidation loans can qualify for forgiveness under certain income-driven repayment plans, including the ICR plan and the SAVE plan.

1. https://khositrangsuc.com/mmoga-find-the-best-small-business-line-of-credit-loan/

3. https://khositrangsuc.com/mmoga-va-loan-pre-approval-your-step-by-step-guide/

5. https://khositrangsuc.com/mmoga-sofi-loan-consolidation-your-guide-to-simplifying-debt/

Q: What is the Parent PLUS loan consolidation loophole?

A: The Parent PLUS loan consolidation loophole allows borrowers to consolidate their loans in a specific way to access more favorable income-driven repayment plans.

Q: How do I consolidate Parent PLUS loans?

A: To consolidate Parent PLUS loans, you must fill out a Direct Consolidation Loan application and submit it to a loan servicer. You can do this online or via paper application.

Q: What repayment plans are available after consolidation?

A: After consolidating Parent PLUS loans, borrowers may choose from various repayment plans, including Standard, Graduated, Extended, and Income-Contingent Repayment (ICR).

By understanding and effectively utilizing these strategies, parents can navigate their financial obligations with confidence, ensuring a more secure future for themselves and their families.

Additional Information and Resources

Navigating the world of student loans can be complex, but there are many resources available to help you along the way. Here are some additional tools and platforms that can assist you in your Parent PLUS loan consolidation journey:

Online Calculators

Utilize online calculators to estimate potential savings from consolidation and different repayment plans. These tools can help you visualize your financial situation and make informed decisions.

Financial Counseling Services

Consider reaching out to financial counseling services that specialize in student loans. These professionals can provide personalized guidance and strategies tailored to your unique financial situation.

Community Support

Engaging with communities on platforms like Reddit or Facebook can provide emotional support and practical tips from those who have experienced similar challenges. Search for groups dedicated to student loans or Parent PLUS loans specifically.

Government Resources

Regularly check the Federal Student Aid website for updates on loan policies, repayment plans, and any new programs that may become available. Staying informed can help you take advantage of new opportunities as they arise.

Educational Workshops

Look for local or online workshops that focus on managing student loans and financial literacy. These can be excellent resources for gaining knowledge and connecting with others facing similar situations.

Consult a Tax Professional

Since student loan debt can have implications for your taxes, consulting a tax professional can provide insights into how your loans may affect your tax situation and what deductions you may qualify for.

By leveraging these resources and staying informed about your options, you can better manage your Parent PLUS loans and work towards financial stability.

Final Thoughts

Navigating Parent PLUS loan consolidation requires diligence and informed decision-making. As you consider your options, remember that you are not alone in this journey. Many parents are facing similar challenges, and there are resources available to help you.

Take the time to explore all avenues for consolidation and repayment, including the potential benefits of the SAVE plan and the double consolidation strategy. Understanding the intricacies of these processes can empower you to make choices that lead to a more secure financial future.

By taking control of your Parent PLUS loan debt today, you can set the stage for a brighter tomorrow for both yourself and your family. Don’t hesitate to seek help, gather information, and utilize available resources. The sooner you act, the closer you’ll be to achieving financial peace of mind.